A fixed deposit (also known as a time deposit) account is a type of bank account that pays account holders a fixed amount of interest in exchange for depositing a certain sum of money for a certain period of time.

Even though fixed deposits offer higher rates than the interest rates offered by most savings accounts, most people do not regard fixed deposit accounts as a form of investment as their interest rates are lower than the inflation rates in Singapore which is estimated to hover around 2.5% to 3.5% annually.

However, that’s not to say that you should immediately write off fixed deposits as a component of your investment portfolio because unlike other forms of investment, fixed deposits are nearly risk free unless the bank collapse. The interest rates are fixed, so you won’t have to worry about market fluctuations. Even if something does happen to the bank, your deposits are still protected, up to $50,000, thanks to the Singapore Deposit Insurance Corporation or SDIC.

If you have a large sum of cash that you don’t intend to spend, putting it in a fixed deposit account will enable you to earn higher interest than if you leave it in a savings account. Interest payments are made like clockwork at regular intervals, often quarterly or annually and fixed deposits are highly liquid. You can withdraw your money anytime, although there may be financial costs to closing your account earlier.

Even though fixed deposits offer higher rates than the interest rates offered by most savings accounts, most people do not regard fixed deposit accounts as a form of investment as their interest rates are lower than the inflation rates in Singapore which is estimated to hover around 2.5% to 3.5% annually.

However, that’s not to say that you should immediately write off fixed deposits as a component of your investment portfolio because unlike other forms of investment, fixed deposits are nearly risk free unless the bank collapse. The interest rates are fixed, so you won’t have to worry about market fluctuations. Even if something does happen to the bank, your deposits are still protected, up to $50,000, thanks to the Singapore Deposit Insurance Corporation or SDIC.

If you have a large sum of cash that you don’t intend to spend, putting it in a fixed deposit account will enable you to earn higher interest than if you leave it in a savings account. Interest payments are made like clockwork at regular intervals, often quarterly or annually and fixed deposits are highly liquid. You can withdraw your money anytime, although there may be financial costs to closing your account earlier.

Property investment is a good way to beat inflation as it offers both rental yield and capital appreciation

Most banks have standard fixed deposit interest rates and because it is usually unattractive, I feel that it is usually not worth my time to open a fixed deposit account unless there’s a good promotion going on. So I saw an article on moneysmart.sg and some bank websites and thought you may want to consider some promotional interest rates for SGD time deposits on the market (subject to changes from banks without prior notice). See below for the best SGD fixed deposit promotional interest rates:

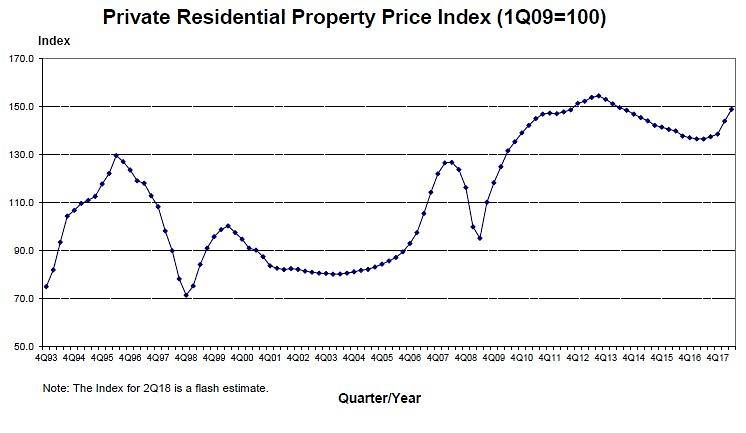

URA's private property price index shows Singapore property is a good investment tool

Maybank Requires minimum of $20,000 deposit for minimum 12 months @ 2.05% p.a.

(with $2,000 deposit in current/savings account)

ICBC Requires min of $20,000 deposit for minimum 12 months @ 1.98% p.a.

(online promotion only)

State Bank of India Requires minimum of $50,000 deposit for 12 months @ 1.95% p.a.

CIMB Requires minimum of $10,000 deposit for 12 months @ 1.9% p.a.

(online only, expires 28 Feb)

ICBC Requires minimum of $20,000 deposit for 9 months @ 1.88% p.a. (online only)

Hong Leong Finance Requires minimum of $50,000 deposit for 13 months @ 1.83% p.a.

Citibank Requires minimum of $50,000 deposit for 6 months @ 1.78% p.a. (expire 28 Feb)

(with $2,000 deposit in current/savings account)

ICBC Requires min of $20,000 deposit for minimum 12 months @ 1.98% p.a.

(online promotion only)

State Bank of India Requires minimum of $50,000 deposit for 12 months @ 1.95% p.a.

CIMB Requires minimum of $10,000 deposit for 12 months @ 1.9% p.a.

(online only, expires 28 Feb)

ICBC Requires minimum of $20,000 deposit for 9 months @ 1.88% p.a. (online only)

Hong Leong Finance Requires minimum of $50,000 deposit for 13 months @ 1.83% p.a.

Citibank Requires minimum of $50,000 deposit for 6 months @ 1.78% p.a. (expire 28 Feb)

Extracted from the blog titled: The Best Fixed Deposit Promotions in Singapore (2019) by Clara Lim on moneysmart.sg

View Upcoming Projects |  Follow Latest News & Property Updates |

RSS Feed

RSS Feed