Around 42 private residential launches, estimated 5,421 units are expected to launch in 2022. Find out more here

The government announced new property curbs on 16 December 2021 to cool its housing market amid rising concern of “prices running ahead of economic fundamentals and increasing risk of a future destabilising correction” after an excellent year for 2021 property market where an estimated 13,000 units were sold by developers, 30.2% higher than 2020. This is the highest annual sales since 2013. Around 10,000 units from 24 private residential projects were launched for sale in 2021 with 12 projects in the CCR, 7 projects in the RCR and 5 projects in the OCR.

This latest round of cooling measures are seen by industry watchers as one of the most aggressive yet. Notably, Additional Buyer Stamp Duties (ABSD) for non-entities have been increased by about 5% to 15% for certain buyer types. This is higher as compared to previous rounds, where the increases ranged from only 5% to 10%. Additionally, the Total Debt Servicing Ratio (TDSR) has been tightened further from 60% to 55% as well as Loan-to- value ratios (LTV) for HDB loans have been reduced from 90% to 85%.

ABSD for foreigners was significantly increased by 10% points to reach 30%. Some consider the increase in ABSD for foreigners to have limited effect, given their small impact as foreign purchases for non-landed private residential properties made up only around 4% of demand for 2020 and 2021.

The increase in ABSD is not expected taper foreign buying demand, especially when borders’ measures are gradually relaxed, leading to the return of overseas buyers. Foreigners’ interest may be diverted to alternative asset classes such as strata retail shops, shophouses or strata offices that do not face or have limited cooling measure risk.

This latest round of cooling measures are seen by industry watchers as one of the most aggressive yet. Notably, Additional Buyer Stamp Duties (ABSD) for non-entities have been increased by about 5% to 15% for certain buyer types. This is higher as compared to previous rounds, where the increases ranged from only 5% to 10%. Additionally, the Total Debt Servicing Ratio (TDSR) has been tightened further from 60% to 55% as well as Loan-to- value ratios (LTV) for HDB loans have been reduced from 90% to 85%.

ABSD for foreigners was significantly increased by 10% points to reach 30%. Some consider the increase in ABSD for foreigners to have limited effect, given their small impact as foreign purchases for non-landed private residential properties made up only around 4% of demand for 2020 and 2021.

The increase in ABSD is not expected taper foreign buying demand, especially when borders’ measures are gradually relaxed, leading to the return of overseas buyers. Foreigners’ interest may be diverted to alternative asset classes such as strata retail shops, shophouses or strata offices that do not face or have limited cooling measure risk.

Piccadilly Grand is an upcoming mixed condo project in Northumberland Road beside Farrer Park MRT & shopping malls jointly developed by 2 heavy weight developers - City Developments (CDL) and MCL Land, exhibiting full confidence in the long-term fundamentals of the Singapore residential market.

The new cooling measures impacts all segments of buyers with tighter loan curbs with higher upfront costs due to a tightening of TDSR and increase in ABSD. First-time Singaporean and Permanent Resident (PR) private residential buyers were the least affected with ABSD rates remaining unchanged.

The impact would be more keenly felt for property investors. Singaporean property buyers now face higher ABSD of 17% and 25% for their 2nd and 3rd property purchase, respectively as compared to 12% and 15% previously. For PRs, they now have to pay 25% and 30% ABSD for their 2nd and 3rd private residential purchase from 15% previously. Coupled with TDSR tightening, investor demand is expected to cool significantly, due to potential higher upfront costs and tighter financing conditions.

The impact would be more keenly felt for property investors. Singaporean property buyers now face higher ABSD of 17% and 25% for their 2nd and 3rd property purchase, respectively as compared to 12% and 15% previously. For PRs, they now have to pay 25% and 30% ABSD for their 2nd and 3rd private residential purchase from 15% previously. Coupled with TDSR tightening, investor demand is expected to cool significantly, due to potential higher upfront costs and tighter financing conditions.

Perched atop the verdant Pearl’s Hill City Park, One Pearl Bank is set to be the tallest residential development in the Outram-Chinatown district in Central Singapore comprising two gently curving 39-storey towers linked at the roof by dramatic sky bridges featuring panoramic views extending from the Central Business District to Sentosa.

The en-bloc market which had just picked up pace in the last couple of months are expected to cool as developers become more selective and wait to see the impact on demand especially when developers are now facing significantly higher development risks given the increase in ABSD for entities. The risks to developers have been increased by 10% to 35% should they fail to sell everything within 5 years. This is onerous on developers and en-bloc hopefuls have to temper their expectations to increase their chances of a successful en-bloc. The higher ABSD rates coupled with ongoing construction uncertainties, and uncertain demand due to the new cooling measures, have increased development risks, especially for large-scale projects.

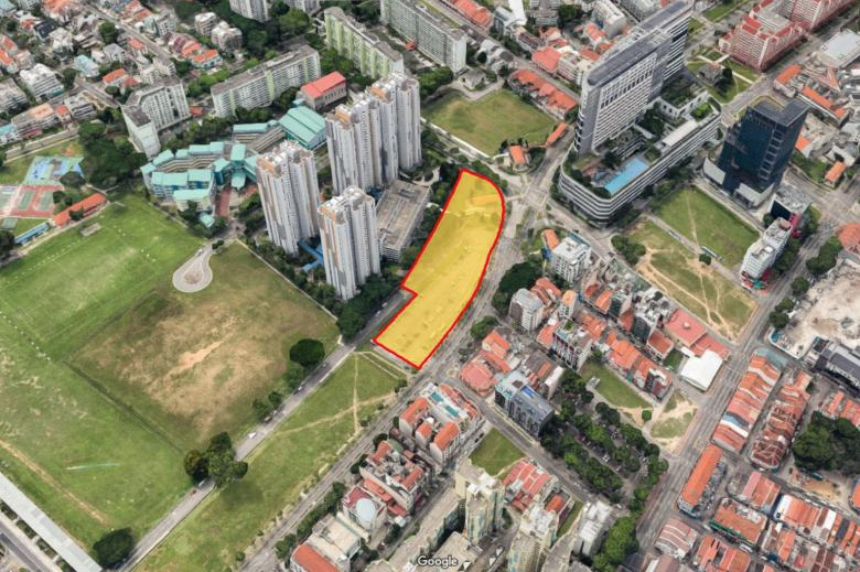

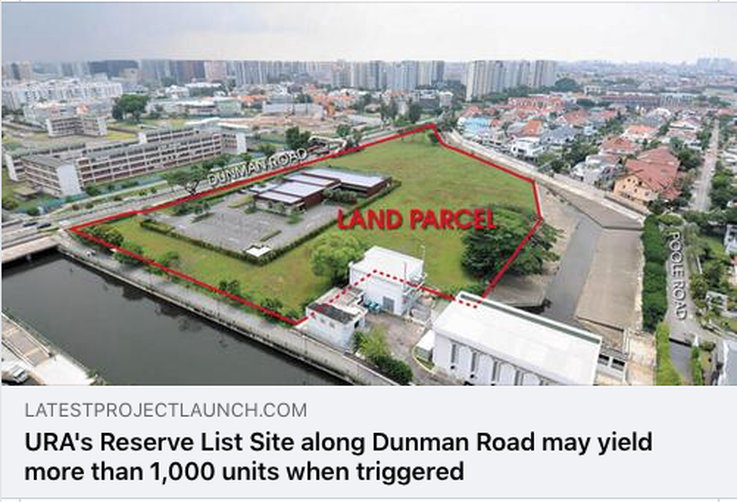

We could still see en-bloc demand for well-located smaller sites at prime districts, where buyers’ profiles tend to be very high net worth and hence may not be too impacted by higher ABSD. As developers need to ensure feasible profit margins, land bid prices are expected to moderate after factoring in higher costs and risks associated. As developers turn towards Government Land Sales (GLS) Programme to fill their empty lan banks, the government is under pressure to release more land to fill the void from en-bloc market to satisfy developer's demand for land. It remains to be seen if the government is more inclined to fill its national reserves or lower their collections from the sale of each plot of GLS if they decide to supply more GLS land. Increased supply will usually lower the bid price submitted by developers.

We could still see en-bloc demand for well-located smaller sites at prime districts, where buyers’ profiles tend to be very high net worth and hence may not be too impacted by higher ABSD. As developers need to ensure feasible profit margins, land bid prices are expected to moderate after factoring in higher costs and risks associated. As developers turn towards Government Land Sales (GLS) Programme to fill their empty lan banks, the government is under pressure to release more land to fill the void from en-bloc market to satisfy developer's demand for land. It remains to be seen if the government is more inclined to fill its national reserves or lower their collections from the sale of each plot of GLS if they decide to supply more GLS land. Increased supply will usually lower the bid price submitted by developers.

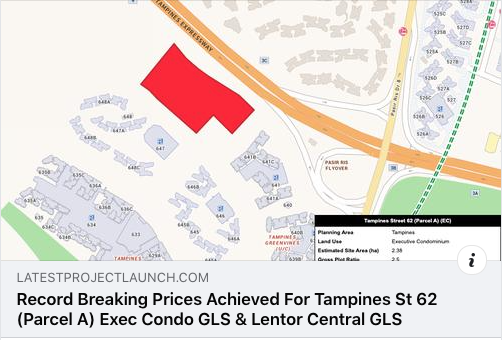

In 2022, sales of new homes will be constrained by the lack of new supply. Around 42 private residential launches are expected consisting of 5,421 units in 2022 with 21.7% in the CCR, 36.4% in the RCR and 41.9 % in the OCR. Two EC projects may be launch in 2022 - North Gaia in Yishun in Mar / Apr 2022 and another along Tengah Garden Walk probably in 4th Qtr 2022. Another EC project along Tam pines Street 62 will reach its 15th month in Nov 2022 and may be launch in 1st Qtr 2023.

Upcoming projects include Belgravia Ace, Kovan Jewel, Royal Hallmark, The Arden, Piccadilly Grand, Gems Ville, Sophia Regency, Evelyn Newton, former 10A/B & 11 Institution Hill, former 2, 4 and 6 Mount Emily Road , former Ji Liang Gardens , projects along Ang Mo Kio Ave 1 and Tanah Merah Kechil Link .

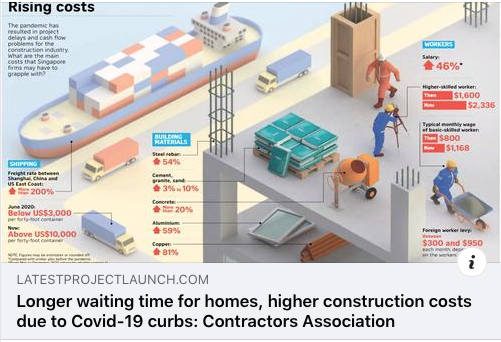

Overall , the new home market may see sales between 8,000 and 9,000 units while prices may move up to 3% in 2022 on the back of higher construction costs.

Kiwi Lim from Huttons Asia believed that due to the current very low levels of unsold inventory, developers will continue sourcing for GLS land and en-bloc smaller residential projects cautiously. Developers are also not expected to cut prices for existing launches as unsold inventory remains very limited and developers have to brace themselves with higher construction costs which may be made even higher with the prospect of an increase in GST this year.

Upcoming projects include Belgravia Ace, Kovan Jewel, Royal Hallmark, The Arden, Piccadilly Grand, Gems Ville, Sophia Regency, Evelyn Newton, former 10A/B & 11 Institution Hill, former 2, 4 and 6 Mount Emily Road , former Ji Liang Gardens , projects along Ang Mo Kio Ave 1 and Tanah Merah Kechil Link .

Overall , the new home market may see sales between 8,000 and 9,000 units while prices may move up to 3% in 2022 on the back of higher construction costs.

Kiwi Lim from Huttons Asia believed that due to the current very low levels of unsold inventory, developers will continue sourcing for GLS land and en-bloc smaller residential projects cautiously. Developers are also not expected to cut prices for existing launches as unsold inventory remains very limited and developers have to brace themselves with higher construction costs which may be made even higher with the prospect of an increase in GST this year.

|  |

|  |

|  |

RSS Feed

RSS Feed