NUS announced on Oct 30 2017 that overall private condominium and apartment prices rose 0.1% month-on-month in September 2017, based on the latest flash values of the Singapore Residential Price Index Series. This marks the fifth straight month of increase in the overall SRPI.

The SRPI Central index saw the strongest growth since April 2017, rising 3.9% over the five-month period. This is due to the limited supply of newly launched private residential homes in the Central Region, which causes buyers to turn to the resale market. In September, the Central index rose 0.4% month-on-month.

The SRPI Non-Central index also saw a 2.1% increase over the same five-month period. The SRPI Small Units index rose just 0.3% over the five month period, but registered the strongest growth for September alone, rising 0.9% month-on-month. These indicate that the Singapore property market is poised for a recovery as investors from Asia turn their focus to Singapore due to our stable government and Singapore's attractive property prices compared with property in their own Asian cities.

The SRPI Central index saw the strongest growth since April 2017, rising 3.9% over the five-month period. This is due to the limited supply of newly launched private residential homes in the Central Region, which causes buyers to turn to the resale market. In September, the Central index rose 0.4% month-on-month.

The SRPI Non-Central index also saw a 2.1% increase over the same five-month period. The SRPI Small Units index rose just 0.3% over the five month period, but registered the strongest growth for September alone, rising 0.9% month-on-month. These indicate that the Singapore property market is poised for a recovery as investors from Asia turn their focus to Singapore due to our stable government and Singapore's attractive property prices compared with property in their own Asian cities.

Park Place Residences is one of the most sought after integrated residential property in Singapore.

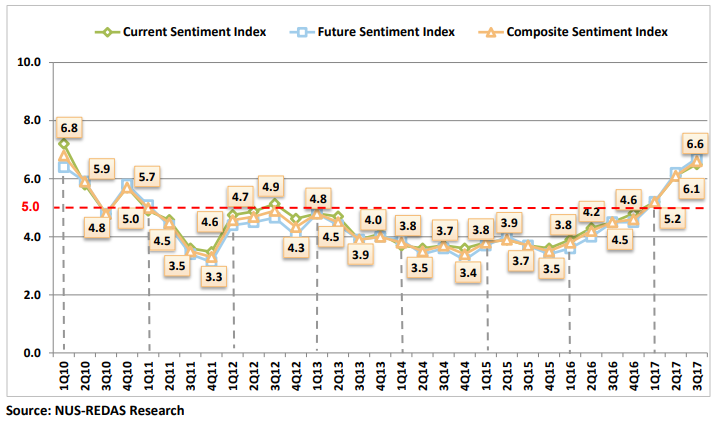

The property market sentiment shows the highest in seven years with overall sentiment for the real estate market standing at 6.6 in 3rd Quarter 2017, a 0.5 point increase quarter-on-quarter from 6.1 in 2nd Quarter 2017, and the highest since 1st Quarter 2010 when it was 6.8, according to the Real Estate Sentiment Index (RESI) released by the National University of Singapore and the Real Estate Developers’ Association of Singapore (REDAS).

Both the property indices reflecting current and future sentiment rose from 2nd Quarter 2017, continuing the uptrend from 4th Quarter 2015. Every quarter of the year, National University of Singapore and REDAS holds a survey among senior executives of REDAS member firms to measure real estate market sentiment in Singapore. A score above 5 indicates improving conditions.

Both the property indices reflecting current and future sentiment rose from 2nd Quarter 2017, continuing the uptrend from 4th Quarter 2015. Every quarter of the year, National University of Singapore and REDAS holds a survey among senior executives of REDAS member firms to measure real estate market sentiment in Singapore. A score above 5 indicates improving conditions.

A score above 5 indicates improving conditions.

Overall prices of completed private apartments and condos in Singapore inched up 0.9% from July to August, based on the latest release of the Singapore Residential Price Index Series by National University of Singapore.

In August, prices for private non-landed homes excluding small units in the central region were up 1%, compared to 0.1% month-on-month increase in July. Prices for private non-landed homes excluding small units in the non-central region also saw a gain of 0.9%, after a 1.1% hike in July. Meanwhile, prices of small units (up to 506 sq ft) climbed 0.3%, following a 0.6% decline in July.

In August, prices for private non-landed homes excluding small units in the central region were up 1%, compared to 0.1% month-on-month increase in July. Prices for private non-landed homes excluding small units in the non-central region also saw a gain of 0.9%, after a 1.1% hike in July. Meanwhile, prices of small units (up to 506 sq ft) climbed 0.3%, following a 0.6% decline in July.

Forest Woods is a highly sought after residential condo within 5 mins walk to NEX. More than 95% sold.

This positive sentiment in Singapore property market is driven by local demand who have already accepted the fact that ABSD is here to stay and also the influx of Chinese investors continuing to shift their focus from the US to Asia, particularly Hong Kong, Singapore and Shanghai - which continue to be the top three investment destinations in Asia.

Fifth straight month of price increases for completed private condos - By Angela Teo / EdgeProp | November 3, 2017 2:55 PM MYT

RSS Feed

RSS Feed