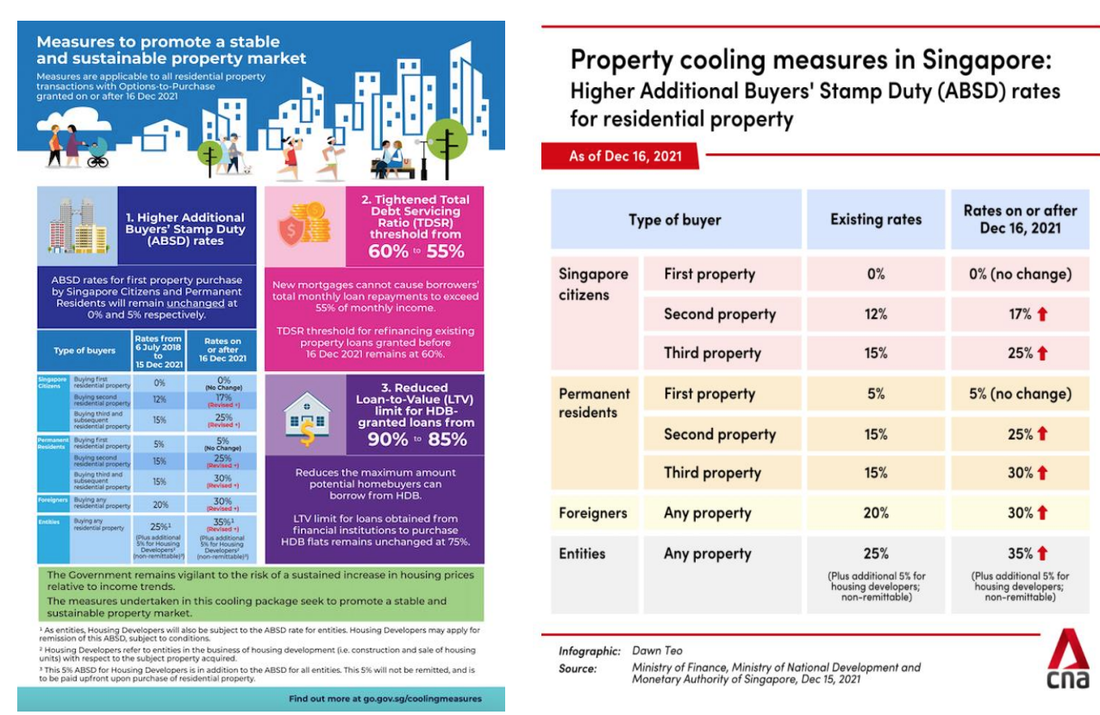

The Government on 15 Dec 2021 (Wednesday) announced a package of measures to cool the private residential and HDB resale markets. The measures include raising Additional Buyer’s Stamp Duty (ABSD) rates, tightening the Total Debt Servicing Ratio (TDSR) threshold and lowering the Loan-to-Value (LTV) limit for loans from the Housing and Development Board (HDB) in an attempt to cool the private and public housing markets are meant to "promote continued housing affordability".

Singapore citizens will now pay an ABSD rate of 17 per cent for their second residential property, and 25 per cent for their third and subsequent residential property. This is up from the previous rate of 12 per cent and 15 per cent respectively. The ABSD rates for permanent residents buying a second or a third and subsequent residential property has been increased to 25 per cent and 30 per cent respectively, up from 15 per cent. Foreigners and entities will also incur more ABSD when purchasing any residential property.

Below are some suggestions on how you can save money on ABSD when buying your 2nd property.

Things to consider where one of the parties is non Singaporean:

a. Who to remain and who to exit

b. If ABSD is payable, consider application for remission

c. Factors to consider where children are involved

Singapore citizens will now pay an ABSD rate of 17 per cent for their second residential property, and 25 per cent for their third and subsequent residential property. This is up from the previous rate of 12 per cent and 15 per cent respectively. The ABSD rates for permanent residents buying a second or a third and subsequent residential property has been increased to 25 per cent and 30 per cent respectively, up from 15 per cent. Foreigners and entities will also incur more ABSD when purchasing any residential property.

Below are some suggestions on how you can save money on ABSD when buying your 2nd property.

Things to consider where one of the parties is non Singaporean:

a. Who to remain and who to exit

b. If ABSD is payable, consider application for remission

c. Factors to consider where children are involved

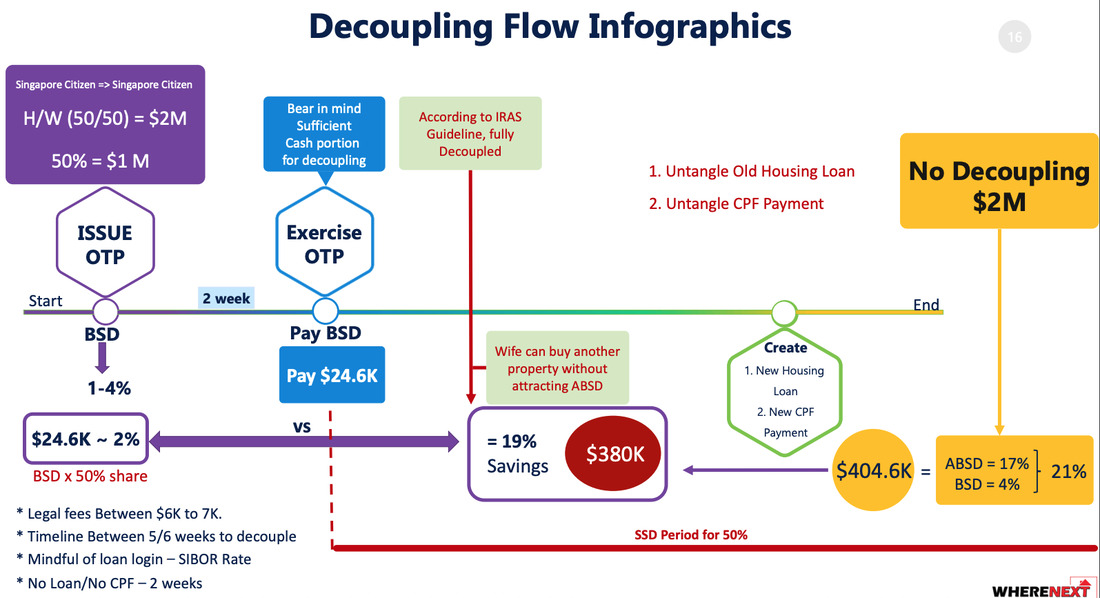

Decoupling

These are some potential costs to be taken into consideration in decoupling:-

•the Transferor may be subject to Seller’s Stamp Duty on the share transferred if the Transferor purchased the property less than 3 years ago;

•ABSD is payable on the value of the share transferred if the Transferee has more than one property;

•if the decoupling transaction is done within the lock-in period for the bank loan, then the bank may charge a penalty;

•if the Transferor had initially used CPF funds in purchasing the property, the CPF funds and accrued interest have to be refunded into his CPF account. Usually, the Transferee would obtain a fresh loan to pay for the purchase of the share transferred in his favour. From the proceeds of the sale, the Transferor would refund his CPF monies, pay for his share of the outstanding bank loan and retain the balance. The fresh loan obtained by the Transferee should be in a quantum that is also sufficient to refinance the Transferee’s own share of outstanding bank loan; and

•the total legal costs will be about $5000 to $6000. For example, Mr. Lee and Mrs. Lee (both Singapore Citizens) had 3 residential properties in their joint names. They wished to upgrade one of the properties to a bigger property. This was their course of action:-

•Sell Property A. Hence, they were left with 2 properties in their joint names;

•Decouple Property B. Mrs. Lee bought Mr. Lee’s share.

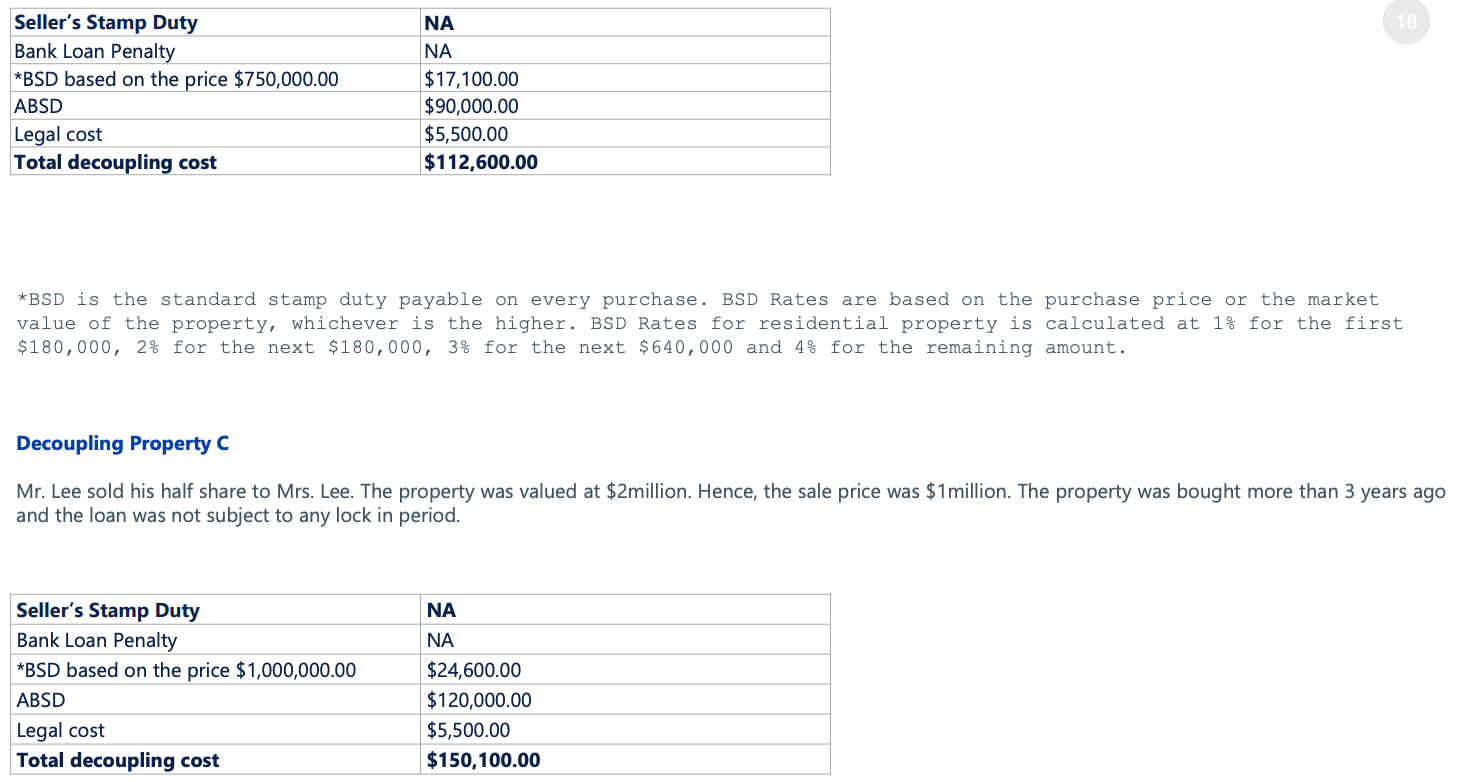

•Decouple Property C. Mrs. Lee bought Mr. Lee ‘s share.

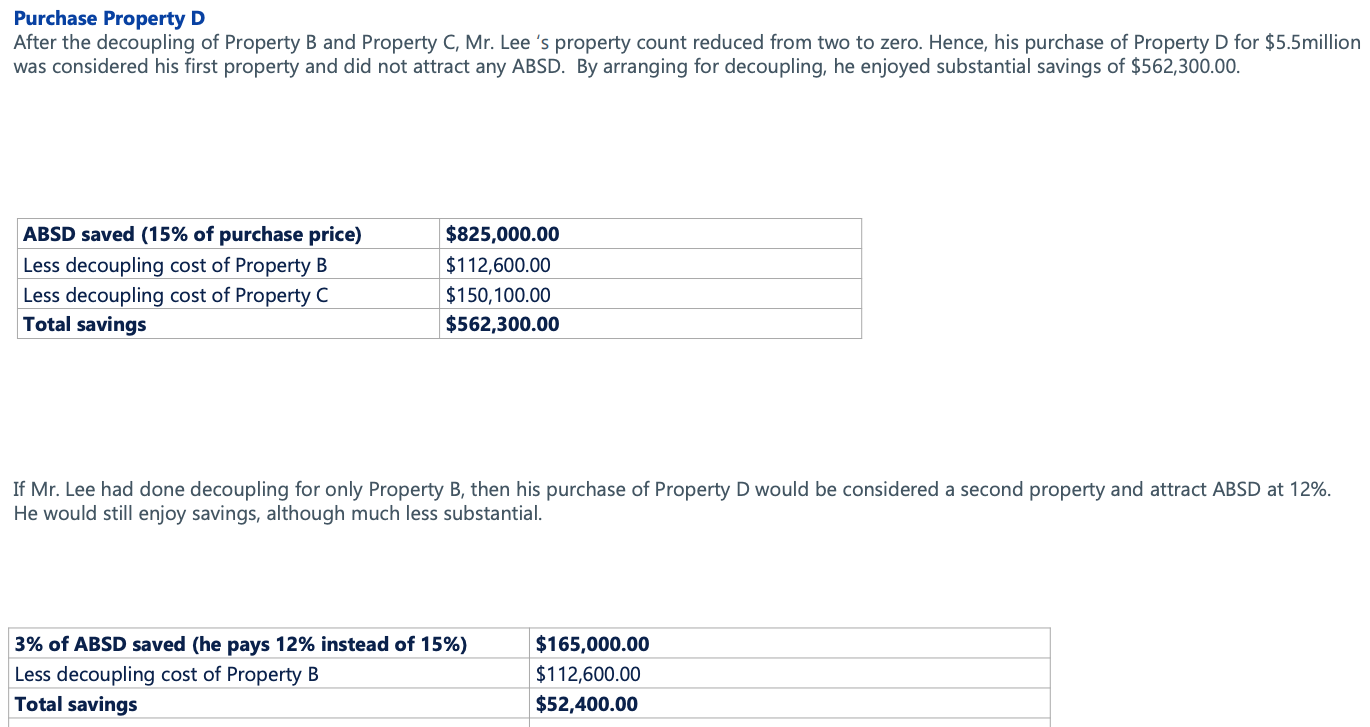

•Mr Lee bought Property D as his 1 st property. Sale of Property A Mr and Mrs Lee sold Property A. After their buyer exercised the option to purchase, Mr and Mrs Lee’s property counts reduced from 3 to 2. Decoupling Property B Mr. Lee sold his half share to Mrs. Lee. The property was valued at $1.5million. Hence, the sale price was $750,000.00. The property was bought more than 3 years ago and the bank loan was not subject to any lock in period.

For More Ideas On How To Save On ABSD, Feel Free To Scan QR Code Below

|

|